- The J Curve

- Posts

- The Anti-Freedom Guide to Financial Products

The Anti-Freedom Guide to Financial Products

Olga Maslikhova

August 21, 2025

I love stories like the one we're about to profile. You know the type: a financially underserved niche that's actually the size of an elephant in the room—tens of millions of Brazilian micro and small enterprises spending hundreds of billions annually, yet somehow invisible to both traditional banks and the first wave of fintechs. I love the platform approach where you start solving one specific pain point, then gradually expand to become the infrastructure layer that entire industries depend on. And I especially love when founders have the conviction to completely pivot their business model at exactly the right moment, even when it means throwing away months of product development.

That's exactly what Andre Bernardes did with Zippi. In just three years, Zippi has gone from a sub-$1M revenue credit card startup to a $55M run-rate payments infrastructure player, serving tens of millions of Brazil’s micro and small entrepreneurs.

But this isn’t just another fintech story. Andre’s thinking on market entry, product design, and competitive positioning offers tactical frameworks that apply far beyond financial services. From his idea of “self-driving finance” to building learning velocity through high-frequency interactions, Zippi’s playbook is relevant to anyone building in fragmented, underserved markets.

The timing makes it even more striking. Just as Brazil’s Pix system was redrawing the country’s payments landscape, Andre made the bold decision to pivot Zippi’s business model. The result was a company that isn’t only serving an underserved market but laying the rails for a new layer of Brazil’s economy.

In this conversation, we dive into the operational frameworks, capital allocation discipline, and long-term strategy behind that growth. Whether you’re in fintech, SaaS, or any B2B market where distribution is fragmented and data is scarce, there are lessons here worth stealing.

Let’s get into it.

EMBRACE WHAT BANKS CALL FRAUD

Olga Maslikhova: When you started Zippi, what did you see as the biggest unmet need?

Andre Bernardes: In Brazil, micro and small businesses are massive—21.5 million entrepreneurs, responsible for nearly half of the country’s workforce and $240B in annual spend. Yet they’ve been invisible to banks and the first wave of fintechs. Why? Because their reality is different: they operate in real time—cash in the morning, restock by afternoon, sell by evening. Traditional banks can’t match that cadence, and fintechs went after consumers or larger businesses instead.

Bruno Lucas, Andre Bernardes and Ludmila Pontremolez, founders of Zippi

OM: How did Pix force you to rethink Zippi’s model?

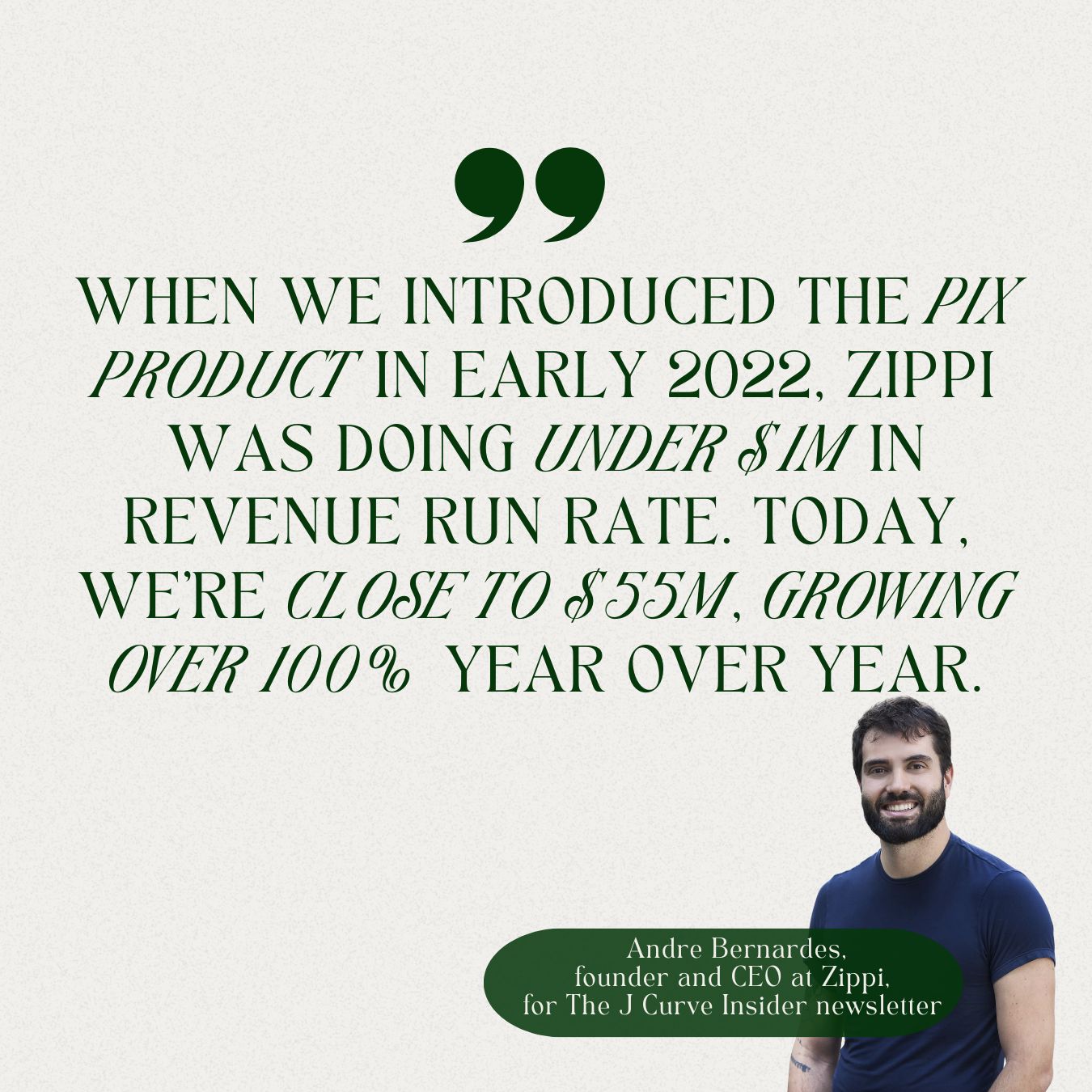

AB: When Brazil’s Central Bank launched Pix in 2021, it was transformational. At the time, Zippi was still a weekly credit card company—already unique compared to the monthly products on the market. But we noticed something unusual: our best customers were swiping their Zippi card into their own POS machines to withdraw cash.

For banks, that looked like fraud. For us, it showed the real job to be done: instant liquidity to restock and sell. So we made a leap— scrapped the credit card, and rebuilt our entire infrastructure on Pix.

When we introduced the Pix product in early 2022, Zippi was doing under $1M in revenue run rate. Today, we’re close to $55M, growing over 100% year over year.

CREDIT IS A GYM, NOT A CASINO

OM: How do you balance rapid growth with portfolio quality?

AB: Credit is like going to the gym—the more reps you do, the fitter you get. Our product is designed for reps. Because Zippi’s loans have a seven-day duration with very high recurrence, the portfolio refreshes constantly. That speed gives us thousands of learning opportunities every month.

The customer base is highly fragmented, which also works in our favor. Lending $500 to 100 people or $50,000 to 100 people gives you the same number of learning cycles—the difference is the value at risk. By keeping loans small and frequent, we get the learning velocity without the blow-ups.

That’s why we built Zippi like a scientific lab: structure the data, run experiments, and improve with every cycle. Over time, that discipline compounds.

Since launch, we’ve:

5x’ed average credit limits

Cut losses by about 40%

Scaled to tens of thousands of customers, with portfolios that fully refresh every week

THE COUNTERINTUITIVE ECONOMICS OF CONSTRAINT

OM: What do you think is most misunderstood about building financial products for micro and small businesses?

AB: Traditional underwriting assumes clean data—income statements, account balances. These businesses don’t have that. Their data is fragmented across personal and business accounts, POS machines, and cash transactions. At Zippi, our job is to treat it like a puzzle—pull the pieces together through open finance and transaction flows—and build credit models that match their reality.

OM: So once you piece the data puzzle together, how do you actually design products for this audience? You’ve described your approach as “self-driving finance.” What does that mean?

AB: A lot of fintechs like to talk about financial freedom—equating success with giving customers as many options as possible. We believe the opposite. The best financial products put guardrails in place so users actually get the outcomes they want, not just the ones they would choose in the moment.

If you give an entrepreneur $1,000 each week, it’s much more payable than a $4,000 bill at the end of the month. The shorter cycle matches their cash flow and actually increases purchase power. By lessening the cycle, you drive better behavior, assess risk more accurately, and create a product that truly fits how these businesses operate.

Image courtesy of Zippi

THE DISCIPLINE OF STRATEGIC SELECTIVITY

OM: What did go-to-market look like for Zippi in the early days?

AB: In our business, the hard part isn't finding customers - our product is bought, not sold. Merchants actively search for credit because they're underserved. The real challenge is knowing who to say yes to.

Most players wait to gather months of data through POS or accounts and only then cross-sell credit. We went the other way: underwrite from day one using alternative signals like cashflow cadence and how many other bank accounts and products they were using.

OM: What's your ideal customer profile today?

AB: The beauty of our strategy is it's horizontal - there's not a specific category that performs better, but a specific job to be done: buying, moving, and selling goods. Our best customers are businesses that require constant operating expenses to operate. Service providers, or retailers who only get paid in 45–60 days, don’t really need a seven-day credit line. The product just doesn’t fit their workflow.

THE CHEAPEST FUNDING IS PROFIT

OM: How did you approach capital allocation after your Series A?

AB: We raised $16M in 2022—right before the market collapsed. From day one, we treated it as if it were the last equity dollar we’d ever raise.

That meant setting one North Star: become profitable. At the time, we were below $1M in revenue run rate and not even gross margin profitable, but the entire company was aligned around efficiency and unit economics.

Our philosophy was simple:

Obsess over unit economics and operational efficiency

Constantly improve LTV to CAC every cycle

Avoid unnecessary hiring—only bring on people who move the needle

From 2022 to today, the team grew from 25 to 66 people—no layoffs, just deliberate hiring paired with heavy investment in technology to drive efficiency.

And the results show: our LTV to CAC was negative at launch. Today, it’s firmly in double digits.

THE AI TRIFECTA

OM: What's the most measurable impact of AI on your operations?

AB: We see AI impact across three layers:

✓ Operations: automating customer support and money movement (FinOps)

✓ Engineering: boosting developer productivity

✓ Analytics: our biggest bet—using AI to supercharge analysts by automating data prep so they focus on hypotheses and experiments

On the customer side, we’re creating conversational collections via natural language, which is far more effective than rigid app flows. Creating app experiences for collections is extremely difficult due to edge cases - each customer needs different parameters based on segmentation. We're creating hyper-specialized user journeys for collections powered by natural language, and it's been a game changer.

THE “CAN I PAY WITH ZIPPI?” ENDGAME

OM: How do you think about moats in the long run?

AB: The big opportunity is to evolve from a unilateral credit product into a payment method for B2B transactions. Small retailers need terms, but their suppliers are also cash-constrained and not built to price or underwrite risk. If Zippi powers that flow, we create three moats:

✓ Distribution moat: suppliers become proprietary acquisition channels

✓ Data moat: supplier–retailer payment data is unique and invisible to the financial system

✓ Economic moat: if suppliers eventually pay for the rails—like merchants pay acquirers—the best customers don’t even need to pay for the credit

Winning for us will be when the whole market runs through Zippi. A small retailer says, “I have Zippi, can I pay through Zippi?” and the wholesaler replies, “Yes, I accept Zippi”—just like credit cards work today.

In that world, the impact on Brazil’s GDP is huge—we’ll enable millions of transactions and make the lives of all these entrepreneurs much better.

RAPID FIRE

OM: What are your non-negotiables in leadership?

AB: The first is the profile we hire for—humble teachers who are also hungry students. People who have the humility to collaborate, teach, and learn, but also the self-awareness to know they don’t know everything and must keep learning. It’s about learning agility, low ego, and collaboration.

The second is radical transparency. Hard truths need to be put on the table from the start. We don’t like political environments or people who distort information.

And the third is raw brainpower. We want to be around people who are extremely smart—people who think faster than we do.

OM: What about decision-making? What is your non-negotiable as a leader in terms of decision-making?

AB: In God we trust. Everyone else must bring data.

OM: What’s one lesson you learned the hard way when it comes to scaling company culture?

AB: If you bring the wrong leader, your culture will implode very fast.

OM: What’s your one piece of advice to founders on structuring their early cap table?

AB: Given the current context of AI, I would try to raise as little as possible and build something very big without raising much equity. I think this is totally doable today.

OM: What’s one trend that’s currently underrated but will have a massive impact on fintech adoption in Brazil?

AB: Conversational banking through WhatsApp. Just as fintechs in 2010–2020 disrupted banks by saying, “No one wants to go to a physical branch anymore, everyone is on their phones and I’m building apps”—what I’m saying is no one wants to be in apps anymore. I don’t want to have to download an app to manage my money. Why would I need to do that? A lot of those financial experiences will be embedded into conversational, social apps that people are already using.

OM: If you had to launch a second startup tomorrow completely outside of credit, what would it be?

AB: I don’t have a good answer because I’m not thinking about other things. But a generic answer would be leveraging AI to solve some sort of critical workflow for B2B.

OM: If Zippi could acquire one company to accelerate growth, what kind of company would it be?

AB: We’re not very acquisitive. It would probably be an acqui-hire of a company that has incredible people working in the domain of data, credit, and financial services.

OM: What’s one global founder you think Brazilian founders can learn the most from?

AB: Max Levchin. What he did with Affirm is very bold. Everyone thinks Affirm is a BNPL company, but that’s not what he’s trying to build—he’s trying to build a new payment network. Two things I admire about him: he’s been relentlessly persistent, working in that domain for years across different companies; and he dreams big. Someone very smart once said, “Dreaming small and dreaming big is the same thing—it’s going to give you the same headache, so you better dream big.” When someone says, “I’m going to build a new payment network,” that is big. That’s something you can’t build overnight.

OM: What’s one team ritual or habit you found surprisingly effective?

AB: Always pre-read documents before synchronous meetings. We try to make async the norm, but when we have to do sync meetings, there has to be a document. Most of our meetings start with 15 minutes of silent reading and commenting, then the rest of the time discussing what needs to be discussed. No presentations, no one just talking through slides—get your ideas down in writing and then we collaborate.

OM: What’s your favorite restaurant in São Paulo?

AB: Cais Restaurant—contemporary cuisine specializing in fresh seafood, an intimate 20-seat setting. I highly recommend the tasting menu.

THE J CURVE HALL OF FAME

Since you made it this far, you might want to check out:

The episode that exploded to 120k+ LinkedIn impressions in just one week and shows no signs of slowing down:

The $1B Pismo Playbook: How Brazilian Startups Beat Silicon Valley at Global Scale

|  |  |

The newsletter issue I keep revisiting: The Consumer Brand Doctors Actually Wear — The complete playbook for guerrilla marketing, community-driven growth, and AI-powered operations that create unbreakable competitive advantages - strategies every founder needs to know.

Thanks for reading,

Olga

P.S. If this issue was valuable to you please share it with a founder who needs to hear it. Let’s build LATAM’s next tech leaders—together

🎙 The J Curve is where LATAM's boldest founders & investors come to talk real strategy, opportunity and leadership.